Table of Contents

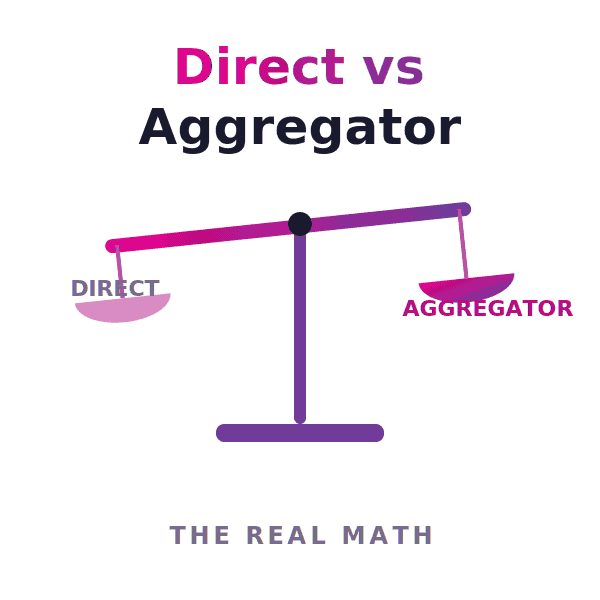

“Go direct and cut out the middleman” sounds like obvious margin. Sometimes it is. Often it costs more than it saves. Here is the honest math on direct supplier contracts versus an aggregator — and the break-even that tells you which to use, supplier by supplier.

There’s a phrase that gets every OTA founder nodding: “cut out the middleman.” Go direct with suppliers, skip the aggregator’s margin, keep the difference. On a whiteboard it’s the obvious move — more margin per booking, a direct relationship, full control. And sometimes it genuinely is the right call.

But “go direct” is a decision people make at the whiteboard and regret at the P&L. Because the margin you save on the rate is real — and so is the cost of building, maintaining, and running that connection, which the whiteboard quietly leaves out. Whether direct actually wins depends entirely on a number most OTAs never calculate.

This is the honest math: what direct genuinely gives you, what it really costs, and the break-even that decides it — supplier by supplier. With the bedbank market heading toward $118.7 billion by 2034 and the number of suppliers worth connecting only rising, getting this decision right per supplier is what separates a healthy margin from a drained one.

A direct supplier contract means you sign commercially with a supplier — a bedbank, a chain, a wholesaler — and integrate their API into your platform yourself. You own the relationship, the rate negotiation, and the connection.

An aggregator (a hotel API aggregator) connects to many suppliers on your behalf and delivers them all through a single API. You integrate once and gain access to everything behind it, with hotel mapping, deduplication, and maintenance handled centrally rather than by your team.

The framing that traps people is treating this as an either/or for your whole business. It isn’t. The decision is made per supplier, and the right answer usually involves both. To make it well, you have to weigh each side honestly — starting with the genuine case for direct.

Let’s be fair to direct — there are real, sometimes decisive advantages, and any honest analysis has to start here.

One supplier represents a large share of your volume; you have a bespoke private-rate contract a third party can’t carry; or you’re large enough that the rate saving on that supplier comfortably exceeds the cost of running the connection. In those cases, direct isn’t just defensible — it’s correct.

Here’s the other side of the ledger — the part the whiteboard leaves off. Going direct doesn’t just cost the rate you save; it costs everything required to build and keep that connection alive, on every supplier you do it for.

A single supplier isn’t one API — it’s six workflows (content, search, pre-book, booking, cancellation, reconciliation), and none standardise across suppliers. A “three-month” build commonly becomes six to nine. Then maintenance never stops: roughly 10–15% of engineering capacity goes to keeping live integrations alive, and that cost is non-linear — manageable at three suppliers, a standing burden at eight, impossible past fifteen. We break this down fully in the hidden cost of integrating suppliers one by one.

There’s more the whiteboard omits: once you have two direct suppliers, hotel mapping and deduplication become your problem. Direct contracts often carry minimum-volume commitments or deposits. And each relationship needs managing. None of this means direct is wrong — it means direct has a real, recurring price per supplier that has to be weighed against the rate saving.

Strip away the ideology and the decision reduces to one comparison, per supplier:

The rate saving side is roughly your volume on that supplier × the per-booking rate advantage. The cost side is the fully-loaded annual cost of that connection: a share of the build amortised, plus maintenance, plus the mapping and failure-handling it adds. When the saving clears the cost, direct pays for itself. When it doesn’t, you’re spending engineering money to lose money.

The reason this matters: the break-even is almost entirely driven by volume on that one supplier. High volume on a single supplier makes the saving large and the per-booking cost of the connection small. Modest volume spread across many suppliers makes the saving small and the per-supplier cost punishing. Which leads directly to how you should actually structure your supply.

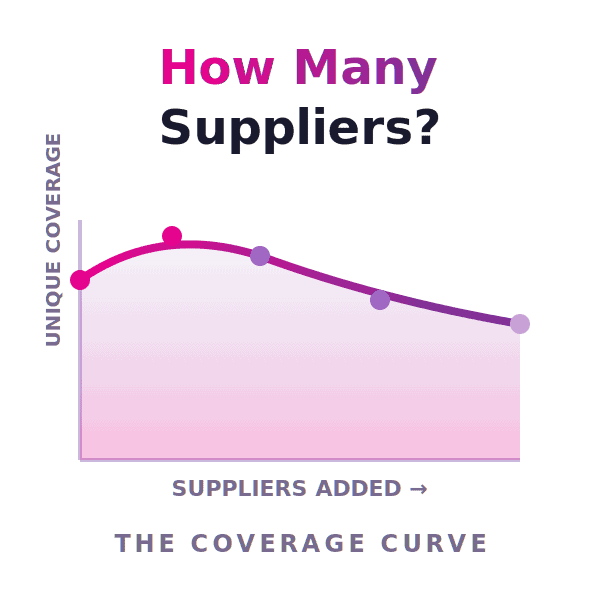

Apply the break-even across your whole supplier list and a pattern emerges that looks a lot like the 80/20 rule. A small handful of suppliers drive most of your bookings; a long tail drive a little each. The two groups give opposite break-even answers.

This is why “all direct” and “all aggregator” are both wrong for most OTAs. All-direct means pouring engineering into long-tail suppliers that never repay it. All-aggregator can mean leaving rate margin on the table for your one or two giant suppliers. The right structure is a portfolio: direct where the break-even clears, aggregator for everything else — and the aggregator is what makes breadth affordable at all. See how the providers compare in our hotel API providers guide.

ZentrumHub connects 100+ suppliers through one API — so you can keep direct deals for your strategic few and let the aggregator handle the rest, with mapping and maintenance included.

See the Universal Hotel API →There’s a common assumption that direct is what you “graduate” to once you’re big enough — that the aggregator is training wheels. The evidence says otherwise. Some of the largest players in travel deliberately run a hybrid, using direct for a strategic few and an aggregator for breadth, because the break-even still favours it even at their scale.

The clearest example: RateHawk — itself a major hotel API that thousands of agencies build on — sources inventory through an aggregator. A company whose entire business is hotel distribution still finds it makes more sense to access part of its supply via aggregation than to build every connection directly. That’s not a company lacking engineering resources; it’s a company that did the math.

The lesson for a growing OTA is freeing: you don’t have to choose direct or aggregator, and you don’t have to “earn” your way off the aggregator. You run the break-even, go direct where it clears, and use the aggregator for everything else — at any size. TravClan grew 4× in daily bookings after freeing its engineers from one-by-one integration to focus on product.

ZentrumHub connects 100+ suppliers through one API — so you keep direct deals where they pay off and let the aggregator handle the long tail, with mapping, maintenance, and failover included. 30M+ daily API calls. 99.99% uptime.

Drop your work email and we’ll send you the 12-page report that breaks down where 6–9 months and $215K+ quietly disappear — free.